Net Burn

Efficiency

Financials

Liquidity

Industry:

Sector Agnostic

Aliases:

Short Definition

Net Burn is the net cash outflow a company experiences over a given period — typically measured monthly. It represents the actual rate at which the company is consuming cash, after accounting for both cash operating expenses and cash inflows from sales or operations. Put simply, it answers: “How much cash are we truly losing each month?” Unlike Gross Burn, which only reflects total spending, Net Burn captures whether revenue or collections are offsetting some of that spend — making it a truer measure of how long the company’s cash will last.

Short Definition

Net Burn is the net cash outflow a company experiences over a given period — typically measured monthly. It represents the actual rate at which the company is consuming cash, after accounting for both cash operating expenses and cash inflows from sales or operations. Put simply, it answers: “How much cash are we truly losing each month?” Unlike Gross Burn, which only reflects total spending, Net Burn captures whether revenue or collections are offsetting some of that spend — making it a truer measure of how long the company’s cash will last.

Why it matters for Investors

Runway predictor: Net Burn directly determines how many months of cash a startup has left before needing new capital. (Runway = Cash Balance ÷ Net Burn)

Efficiency gauge: Reveals whether a startup is scaling responsibly — growing faster than it’s burning.

Liquidity signal: Shows if the company can self-fund operations or is dependent on external financing.

Fundraising input: Investors use Net Burn to estimate how large the next round must be and when it’s needed.

Why it matters for Investors

Runway predictor: Net Burn directly determines how many months of cash a startup has left before needing new capital. (Runway = Cash Balance ÷ Net Burn)

Efficiency gauge: Reveals whether a startup is scaling responsibly — growing faster than it’s burning.

Liquidity signal: Shows if the company can self-fund operations or is dependent on external financing.

Fundraising input: Investors use Net Burn to estimate how large the next round must be and when it’s needed.

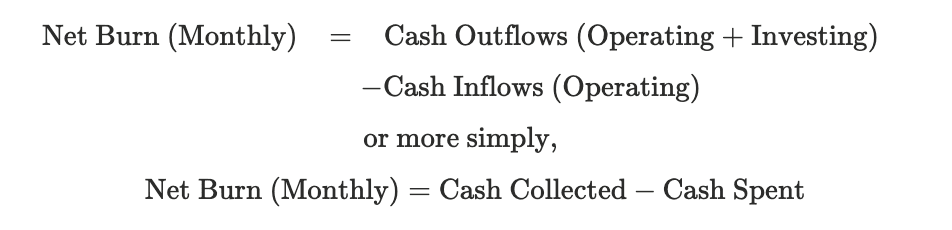

Formula

where:

Cash Outflows = payroll, rent, marketing, vendor costs, tools, etc.

Cash Inflows = customer collections (cash actually received).

Exclude fundraising, debt, or investor inflows (these extend runway but don’t improve burn efficiency).

Practical considerations:

Use cash, not accrual: Base it on actual cash movements — exclude non-cash expenses like depreciation or stock comp.

Exclude financing flows: Don’t count equity raises, debt inflows, or interest income; Net Burn reflects core operations, not fundraising.

Seasonality matters: SaaS or consumer businesses may have uneven cash collections — use rolling averages for truer trends.

Time granularity: Monthly Net Burn is standard; quarterly helps smooth timing noise.

Investor use: Combine with cash balance to calculate runway = cash on hand ÷ net burn.

Formula

where:

Cash Outflows = payroll, rent, marketing, vendor costs, tools, etc.

Cash Inflows = customer collections (cash actually received).

Exclude fundraising, debt, or investor inflows (these extend runway but don’t improve burn efficiency).

Practical considerations:

Use cash, not accrual: Base it on actual cash movements — exclude non-cash expenses like depreciation or stock comp.

Exclude financing flows: Don’t count equity raises, debt inflows, or interest income; Net Burn reflects core operations, not fundraising.

Seasonality matters: SaaS or consumer businesses may have uneven cash collections — use rolling averages for truer trends.

Time granularity: Monthly Net Burn is standard; quarterly helps smooth timing noise.

Investor use: Combine with cash balance to calculate runway = cash on hand ÷ net burn.

Worked Example

Line Item | Monthly Amount | Notes |

|---|---|---|

Cash Inflows from Customers | $400,000 | Cash collected from sales or invoices paid by customers |

Cash Operating Expenses | $1,000,000 | Payroll, rent, software tools, vendors, and other recurring outflows |

Cash Investing Activities | $50,000 | Recurring CapEx — equipment, laptops, small R&D prototypes |

Net Burn (Monthly) | = ($1,000,000 + $50,000 - $400,000) | Formula: Outflows + CapEx − Inflows |

Net Burn = 650,000 | The company is burning $650K per month — the rate at which operations consume cash |

If current cash balance = $5,200,000

→ Runway = $5,200,000 ÷ $650,000 ≈ 8.0 months

The company has roughly 8 months of runway assuming burn stays constant and no new funding or major inflows occur.

Notes:

Burn excludes financing: Equity raises, debt draws, and other CFF items do not reduce burn. They change the cash balance, not operational efficiency.

Burn is cash-based: Use collections (cash received) and cash payments (payroll, vendors). Ignore accrual-only P&L items (depreciation, stock comp).

Recurring CapEx belongs in burn; one-offs don’t: Include recurring operational CapEx (e.g., laptops each month). Exclude large, one-off investing items (e.g., a $500K office build-out) when reporting core Net Burn; disclose them separately.

Reconcile with the cash flow statement: Cash Change=CFO+CFI+CFF. Burn explains the operating + recurring investing part of that movement; financing explains the rest.

Labeling convention: Report Net Burn as a positive number (e.g., “$650K burn”) even though it’s an outflow.

Worked Example

Line Item | Monthly Amount | Notes |

|---|---|---|

Cash Inflows from Customers | $400,000 | Cash collected from sales or invoices paid by customers |

Cash Operating Expenses | $1,000,000 | Payroll, rent, software tools, vendors, and other recurring outflows |

Cash Investing Activities | $50,000 | Recurring CapEx — equipment, laptops, small R&D prototypes |

Net Burn (Monthly) | = ($1,000,000 + $50,000 - $400,000) | Formula: Outflows + CapEx − Inflows |

Net Burn = 650,000 | The company is burning $650K per month — the rate at which operations consume cash |

If current cash balance = $5,200,000

→ Runway = $5,200,000 ÷ $650,000 ≈ 8.0 months

The company has roughly 8 months of runway assuming burn stays constant and no new funding or major inflows occur.

Notes:

Burn excludes financing: Equity raises, debt draws, and other CFF items do not reduce burn. They change the cash balance, not operational efficiency.

Burn is cash-based: Use collections (cash received) and cash payments (payroll, vendors). Ignore accrual-only P&L items (depreciation, stock comp).

Recurring CapEx belongs in burn; one-offs don’t: Include recurring operational CapEx (e.g., laptops each month). Exclude large, one-off investing items (e.g., a $500K office build-out) when reporting core Net Burn; disclose them separately.

Reconcile with the cash flow statement: Cash Change=CFO+CFI+CFF. Burn explains the operating + recurring investing part of that movement; financing explains the rest.

Labeling convention: Report Net Burn as a positive number (e.g., “$650K burn”) even though it’s an outflow.

Best Practices

Exclude financing events: Segregate operational cash flow from VC raises or loans to assess true self-sustainability.

Reconcile to cash balance: Always cross-check with actual bank balances to prevent reporting errors.

Contextualize with revenue: Pair Net Burn with Revenue Growth Rate or ARR to assess burn efficiency.

Monitor trend vs. plan: Flag deviations early — a rising Net Burn without faster growth signals inefficiency.

Best Practices

Exclude financing events: Segregate operational cash flow from VC raises or loans to assess true self-sustainability.

Reconcile to cash balance: Always cross-check with actual bank balances to prevent reporting errors.

Contextualize with revenue: Pair Net Burn with Revenue Growth Rate or ARR to assess burn efficiency.

Monitor trend vs. plan: Flag deviations early — a rising Net Burn without faster growth signals inefficiency.

FAQs

What’s the difference between Net Burn and Gross Burn?

Gross Burn shows total cash spent, while Net Burn subtracts inflows to show net cash lost. Gross Burn is total monthly cash outflow (spending) before considering any inflows. Net Burn = Gross Burn − Cash Inflows. It reflects your net monthly cash loss.Should we include financing cash flows?

No — exclude inflows from fundraising, debt issuance, or interest income. Net Burn focuses on operational sustainability.Can Net Burn be negative?

Yes — when inflows exceed outflows (e.g., profitable months). That’s called Net Cash Generation or being cash flow positive.Why do investors care more about Net Burn than P&L losses?

Because startups live or die by cash. Profit/loss (on an accrual basis) may look fine, but if cash is dwindling, the runway shortens — and the raise risk grows.

FAQs

What’s the difference between Net Burn and Gross Burn?

Gross Burn shows total cash spent, while Net Burn subtracts inflows to show net cash lost. Gross Burn is total monthly cash outflow (spending) before considering any inflows. Net Burn = Gross Burn − Cash Inflows. It reflects your net monthly cash loss.Should we include financing cash flows?

No — exclude inflows from fundraising, debt issuance, or interest income. Net Burn focuses on operational sustainability.Can Net Burn be negative?

Yes — when inflows exceed outflows (e.g., profitable months). That’s called Net Cash Generation or being cash flow positive.Why do investors care more about Net Burn than P&L losses?

Because startups live or die by cash. Profit/loss (on an accrual basis) may look fine, but if cash is dwindling, the runway shortens — and the raise risk grows.

Related Metrics

Commonly mistaken for:

Gross Burn (Ignores inflows)

Operating Loss (P&L number, not cash-based)

Net Cash Flow (Includes financing and investing)

Related Metrics

Commonly mistaken for:

Gross Burn (Ignores inflows)

Operating Loss (P&L number, not cash-based)

Net Cash Flow (Includes financing and investing)

Index