Net Income

Financials

Industry:

Sector Agnostic

Short Definition

Net Income is the total earnings (or loss) of a company after deducting all operating expenses, interest, taxes, depreciation, amortization, and other costs from total revenue over a specific period. It represents the “bottom line” of the income statement, showing what remains for shareholders after all obligations are met.

Short Definition

Net Income is the total earnings (or loss) of a company after deducting all operating expenses, interest, taxes, depreciation, amortization, and other costs from total revenue over a specific period. It represents the “bottom line” of the income statement, showing what remains for shareholders after all obligations are met.

Why it matters for Investors

Clear profitability signal: Net Income shows whether a business is generating actual profit after all costs, making it a fundamental measure of performance for any stakeholder.

Indicator of value creation: Sustainable, growing net income supports higher company valuations and the capacity to reinvest or distribute returns.

Basis for key ratios: Measures like Earnings Per Share (EPS), Price/Earnings (P/E), and Return on Equity (ROE) rely on Net Income, making it central for benchmarking and investor analysis.

Why it matters for Investors

Clear profitability signal: Net Income shows whether a business is generating actual profit after all costs, making it a fundamental measure of performance for any stakeholder.

Indicator of value creation: Sustainable, growing net income supports higher company valuations and the capacity to reinvest or distribute returns.

Basis for key ratios: Measures like Earnings Per Share (EPS), Price/Earnings (P/E), and Return on Equity (ROE) rely on Net Income, making it central for benchmarking and investor analysis.

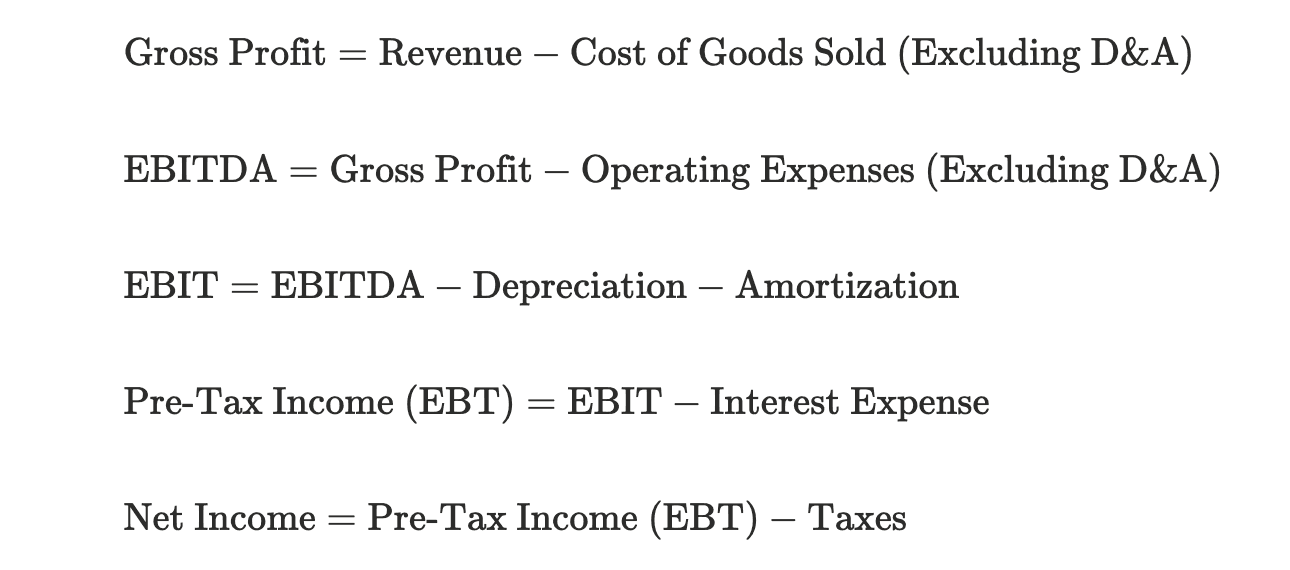

Formula

Notes:

Operating Expenses (OpEx) do not include Depreciation & Amortization (D&A) in this formula. This is because D&A are non-cash expenses typically embedded within specific operating expense line items (like Research & Development, Sales & Marketing, or General & Administrative Expenses) in standard financial statements.

For clear analysis and EBITDA calculation, it's essential to separate out D&A from OpEx since EBITDA is earnings before these non-cash charges.

Practical considerations:

Understand the context of negative net income: Many startups show negative net income initially due to heavy investments in product development, marketing, and talent acquisition. This is normal and not always a sign of failure but requires careful monitoring of growth and burn rate.

Focus on growth trajectory: Investors look for net income moving toward positive over time, indicating a path to profitability. Founders should aim to improve operational efficiency and manage expenses to bend the curve toward profitability.

Look beyond the bottom line: Net income alone doesn't tell the full story. Combine it with other metrics like cash flow, burn rate, customer acquisition cost, and lifetime value to get a holistic view of financial health.

Liquidity assessment: Since net income is accrual-based, founders and investors should always compare it with cash flow statements to understand the company’s true liquidity and runway.

Analyze operating efficiency: Net income margin (net income as a percentage of revenue) helps assess how well the startup converts sales into profit, vital for assessing scalability and sustainability.

Accrual vs. Cash Timing: Net income is based on accrual accounting, recognizing revenues and expenses when earned or incurred, not necessarily when cash is received or paid. Early-stage founders should be aware that this can create differences between reported profitability and actual cash flow, so net income should be analyzed in conjunction with cash flow statements for liquidity assessment.

Important Variants:

Adjusted Net Income: Adjusted Net Income starts with reported net income and then normalizes it by adding back non-cash charges (like depreciation), one-time gains or losses, stock-based compensation, restructuring costs, and any unusual expenses not expected to recur. This adjusted figure gives a clearer picture of a startup's ongoing profitability and operational health, helping investors understand the core earnings potential without noise from infrequent or accounting-driven items. It is especially useful for valuation and performance comparisons.

GAAP Net Income: GAAP Net Income is Net Income calculated strictly according to official accounting rules called Generally Accepted Accounting Principles (GAAP). These rules ensure every company reports income in a consistent and transparent way, making it easier for investors to compare businesses. GAAP Net Income is the official, audited profit figure that companies report to regulators and investors.

Formula

Notes:

Operating Expenses (OpEx) do not include Depreciation & Amortization (D&A) in this formula. This is because D&A are non-cash expenses typically embedded within specific operating expense line items (like Research & Development, Sales & Marketing, or General & Administrative Expenses) in standard financial statements.

For clear analysis and EBITDA calculation, it's essential to separate out D&A from OpEx since EBITDA is earnings before these non-cash charges.

Practical considerations:

Understand the context of negative net income: Many startups show negative net income initially due to heavy investments in product development, marketing, and talent acquisition. This is normal and not always a sign of failure but requires careful monitoring of growth and burn rate.

Focus on growth trajectory: Investors look for net income moving toward positive over time, indicating a path to profitability. Founders should aim to improve operational efficiency and manage expenses to bend the curve toward profitability.

Look beyond the bottom line: Net income alone doesn't tell the full story. Combine it with other metrics like cash flow, burn rate, customer acquisition cost, and lifetime value to get a holistic view of financial health.

Liquidity assessment: Since net income is accrual-based, founders and investors should always compare it with cash flow statements to understand the company’s true liquidity and runway.

Analyze operating efficiency: Net income margin (net income as a percentage of revenue) helps assess how well the startup converts sales into profit, vital for assessing scalability and sustainability.

Accrual vs. Cash Timing: Net income is based on accrual accounting, recognizing revenues and expenses when earned or incurred, not necessarily when cash is received or paid. Early-stage founders should be aware that this can create differences between reported profitability and actual cash flow, so net income should be analyzed in conjunction with cash flow statements for liquidity assessment.

Important Variants:

Adjusted Net Income: Adjusted Net Income starts with reported net income and then normalizes it by adding back non-cash charges (like depreciation), one-time gains or losses, stock-based compensation, restructuring costs, and any unusual expenses not expected to recur. This adjusted figure gives a clearer picture of a startup's ongoing profitability and operational health, helping investors understand the core earnings potential without noise from infrequent or accounting-driven items. It is especially useful for valuation and performance comparisons.

GAAP Net Income: GAAP Net Income is Net Income calculated strictly according to official accounting rules called Generally Accepted Accounting Principles (GAAP). These rules ensure every company reports income in a consistent and transparent way, making it easier for investors to compare businesses. GAAP Net Income is the official, audited profit figure that companies report to regulators and investors.

Worked Example

Line Item | Amount | Notes |

|---|---|---|

Revenue | $100,000 | Total sales/income |

(-) Cost of Goods Sold (Excludes D&A) | $(40,000) | Direct costs to produce goods |

= Gross Profit | $60,000 | Revenue minus COGS |

(-) Operating Expenses (Excludes D&A) | $(20,000) | Expenses for running business (salaries, rent, etc.) |

= EBITDA | $40,000 | Earnings before interest, taxes, depreciation & amortization |

(-) Depreciation & Amort. | $(5,000) | Non-cash charges reflecting asset usage |

= EBIT (Operating Income) | $35,000 | Earnings before interest and taxes |

(-) Interest Expense | $(3,000) | Cost of debt |

= EBT (Earnings Before Tax) | $32,000 | Profit before tax |

(-) Taxes | $(7,000) | Income taxes |

= Net Income or PAT | $25,000 | Bottom line profit after all expenses |

Notes:

The waterfall shows how revenue is “waterfalled” down by subtracting costs and expenses step by step until the final net income.

EBITDA is an operational profitability measure before non-cash and financing costs.

PAT (Profit After Tax) is the final net income value available to shareholders.

This waterfall format helps visualize the impact of each cost component on profitability.

Visualizing this stepwise flow helps founders identify cost areas to optimize and enables investors to analyze margin quality and financial efficiency.

Use this structure consistently in reporting to improve transparency and facilitate direct comparisons across periods or peer benchmarks.

Worked Example

Line Item | Amount | Notes |

|---|---|---|

Revenue | $100,000 | Total sales/income |

(-) Cost of Goods Sold (Excludes D&A) | $(40,000) | Direct costs to produce goods |

= Gross Profit | $60,000 | Revenue minus COGS |

(-) Operating Expenses (Excludes D&A) | $(20,000) | Expenses for running business (salaries, rent, etc.) |

= EBITDA | $40,000 | Earnings before interest, taxes, depreciation & amortization |

(-) Depreciation & Amort. | $(5,000) | Non-cash charges reflecting asset usage |

= EBIT (Operating Income) | $35,000 | Earnings before interest and taxes |

(-) Interest Expense | $(3,000) | Cost of debt |

= EBT (Earnings Before Tax) | $32,000 | Profit before tax |

(-) Taxes | $(7,000) | Income taxes |

= Net Income or PAT | $25,000 | Bottom line profit after all expenses |

Notes:

The waterfall shows how revenue is “waterfalled” down by subtracting costs and expenses step by step until the final net income.

EBITDA is an operational profitability measure before non-cash and financing costs.

PAT (Profit After Tax) is the final net income value available to shareholders.

This waterfall format helps visualize the impact of each cost component on profitability.

Visualizing this stepwise flow helps founders identify cost areas to optimize and enables investors to analyze margin quality and financial efficiency.

Use this structure consistently in reporting to improve transparency and facilitate direct comparisons across periods or peer benchmarks.

Best Practices

Regularly reconcile net income with cash flow: Ensure understanding of differences between accrual net income and actual cash generated, as cash is critical for startup survival.

Disclose and analyze adjustments transparently: When presenting adjusted net income, clearly itemize exclusions and rationale to maintain trust and comparability.

Track net income trends over multiple periods: Focus on sustained improvement or stability rather than short-term fluctuations to gauge true financial health and trajectory.

Benchmark against peers and industry averages: Use net income margins and growth relative to similar startups to contextualize performance and identify potential risks or advantages.

Integrate qualitative factors: Combine net income analysis with product-market fit, customer retention, and competitive position to make well-rounded investment or management decisions.

Prepare for due diligence with thorough documentation: Keep detailed records supporting reported net income figures, including adjustments, to facilitate smooth investor audits and funding processes.

Use scenario analysis and forecasting: Model different growth, cost, and funding scenarios to understand net income sensitivity and plan strategic actions proactively.

Align net income goals with overall business strategy: Ensure profit targets reflect long-term vision and growth priorities rather than short-term accounting achievements.

Best Practices

Regularly reconcile net income with cash flow: Ensure understanding of differences between accrual net income and actual cash generated, as cash is critical for startup survival.

Disclose and analyze adjustments transparently: When presenting adjusted net income, clearly itemize exclusions and rationale to maintain trust and comparability.

Track net income trends over multiple periods: Focus on sustained improvement or stability rather than short-term fluctuations to gauge true financial health and trajectory.

Benchmark against peers and industry averages: Use net income margins and growth relative to similar startups to contextualize performance and identify potential risks or advantages.

Integrate qualitative factors: Combine net income analysis with product-market fit, customer retention, and competitive position to make well-rounded investment or management decisions.

Prepare for due diligence with thorough documentation: Keep detailed records supporting reported net income figures, including adjustments, to facilitate smooth investor audits and funding processes.

Use scenario analysis and forecasting: Model different growth, cost, and funding scenarios to understand net income sensitivity and plan strategic actions proactively.

Align net income goals with overall business strategy: Ensure profit targets reflect long-term vision and growth priorities rather than short-term accounting achievements.

FAQs

Is Net Income the same as cash flow?

No. Net income includes non-cash items. Only cash flow from operations shows actual cash generated in a period.Can Net Income be negative?

Yes. This is called a net loss and is common for early-stage or high-investment startups.What’s the difference between Net Income and Operating Income?

Operating Income (EBIT) is profit from operations before interest and taxes. Net Income deducts all remaining costs, including interest and taxes.Are dividends paid out of Net Income?

Yes, but only if the board declares them, and after all other obligations are met.Should founders focus solely on net income?

No. Net income is important but should be balanced with cash flow, customer metrics, and growth indicators for a full business picture.

FAQs

Is Net Income the same as cash flow?

No. Net income includes non-cash items. Only cash flow from operations shows actual cash generated in a period.Can Net Income be negative?

Yes. This is called a net loss and is common for early-stage or high-investment startups.What’s the difference between Net Income and Operating Income?

Operating Income (EBIT) is profit from operations before interest and taxes. Net Income deducts all remaining costs, including interest and taxes.Are dividends paid out of Net Income?

Yes, but only if the board declares them, and after all other obligations are met.Should founders focus solely on net income?

No. Net income is important but should be balanced with cash flow, customer metrics, and growth indicators for a full business picture.

Related Metrics

Commonly mistaken for:

EBITDA (Adds back Interest, taxes, depreciation)

EBIT (Before interest and taxes)

Gross Profit (Before operating expenses)

Related Metrics

Commonly mistaken for:

EBITDA (Adds back Interest, taxes, depreciation)

EBIT (Before interest and taxes)

Gross Profit (Before operating expenses)

Source of:

Components:

Index