Current Liabilities

Financials

Industry:

Sector Agnostic

Short Definition

Current liabilities are the company’s short‑term financial obligations — debts, payables, and other commitments that must be settled within 12 months (or within the normal operating cycle, if longer). Examples include accounts payable, short‑term loans and credit lines, current portions of long‑term debt, accrued expenses, taxes payable, payroll liabilities, and current lease obligations. They represent near‑term cash outflows and are a key measure of liquidity and working‑capital health.

Short Definition

Current liabilities are the company’s short‑term financial obligations — debts, payables, and other commitments that must be settled within 12 months (or within the normal operating cycle, if longer). Examples include accounts payable, short‑term loans and credit lines, current portions of long‑term debt, accrued expenses, taxes payable, payroll liabilities, and current lease obligations. They represent near‑term cash outflows and are a key measure of liquidity and working‑capital health.

Why it matters for Investors

Liquidity signal: Indicates how easily the company can meet short‑term obligations with current assets — a vital input to solvency and runway analysis.

Operating discipline: Growing payables and accrued liabilities can show tight cash management or, conversely, emerging strain if payments are delayed.

Runway realism: For startups, accounts payable and short‑term liabilities often fund part of operating burn — understanding their timing helps investors assess true cash runway.

Risk alert: High current liabilities relative to current assets signal potential liquidity pressure and upcoming refinancing or vendor risks.

Working‑capital driver: Changes in current liabilities directly affect Cash Flow from Operations — a critical insight for investors tracking burn or free‑cash‑flow conversion.

Why it matters for Investors

Liquidity signal: Indicates how easily the company can meet short‑term obligations with current assets — a vital input to solvency and runway analysis.

Operating discipline: Growing payables and accrued liabilities can show tight cash management or, conversely, emerging strain if payments are delayed.

Runway realism: For startups, accounts payable and short‑term liabilities often fund part of operating burn — understanding their timing helps investors assess true cash runway.

Risk alert: High current liabilities relative to current assets signal potential liquidity pressure and upcoming refinancing or vendor risks.

Working‑capital driver: Changes in current liabilities directly affect Cash Flow from Operations — a critical insight for investors tracking burn or free‑cash‑flow conversion.

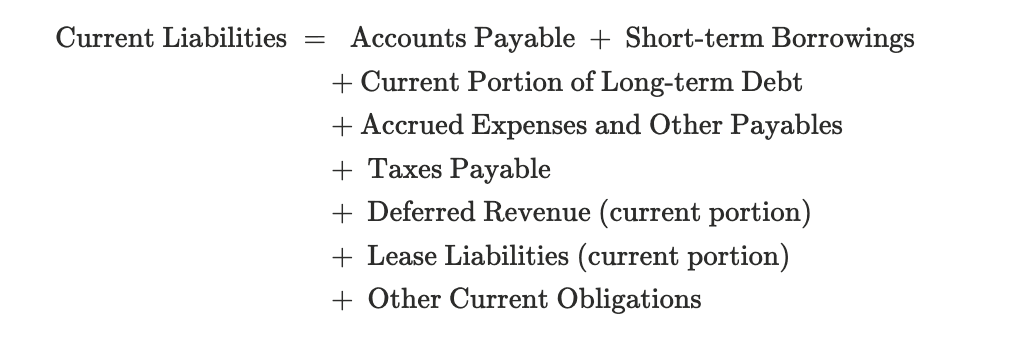

Formula

Practical considerations:

12‑month rule: Any obligation expected to be paid or settled within 12 months (or the standard operating cycle, if longer) is current.

Current portion of long‑term debt: Always separate the next 12 months of principal payments from the rest — this sharpen insight into near‑term cash commitments.

Accruals: Include accrued interest, payroll, taxes, or bonuses earned but not yet paid.

Deferred revenue: The revenue tied to deliverables due within a year (e.g., prepaid subscriptions for the next 12 months).

Operating cycle nuance: If production‑to‑collection lasts longer than 12 months (e.g., infrastructure projects), classify liabilities maturing in that cycle as current.

Reclassification trigger: When a loan breaches covenants or lacks a deferment right at the reporting date, that balance must move from non‑current to current — even if renegotiated later.

Formula

Practical considerations:

12‑month rule: Any obligation expected to be paid or settled within 12 months (or the standard operating cycle, if longer) is current.

Current portion of long‑term debt: Always separate the next 12 months of principal payments from the rest — this sharpen insight into near‑term cash commitments.

Accruals: Include accrued interest, payroll, taxes, or bonuses earned but not yet paid.

Deferred revenue: The revenue tied to deliverables due within a year (e.g., prepaid subscriptions for the next 12 months).

Operating cycle nuance: If production‑to‑collection lasts longer than 12 months (e.g., infrastructure projects), classify liabilities maturing in that cycle as current.

Reclassification trigger: When a loan breaches covenants or lacks a deferment right at the reporting date, that balance must move from non‑current to current — even if renegotiated later.

Worked Example

Current Liability Item | Amount | What It Represents |

|---|---|---|

Accounts Payable | $2,100,000 | Outstanding supplier invoices for goods/services already received |

Short-term Borrowings | $1,800,000 | Revolving credit lines and overdrafts due within 12 months |

Current Portion of Long-term Debt | $900,000 | Principal repayments on term loans due this year |

Accrued Expenses | $650,000 | Accrued bonuses, payroll, utilities, and interest payable |

Taxes Payable | $300,000 | Corporate, payroll, or sales taxes owed but unpaid |

Deferred Revenue (current) | $450,000 | Customer prepayments for services to be delivered within 12 months |

Current Lease Liabilities | $200,000 | Lease payments due in the next 12 months |

Other Current Liabilities | $150,000 | Miscellaneous short-term obligations (e.g., legal or warranty claims) |

Total Current Liabilities | $6,550,000 | Commitments due within the next year |

Notes:

Snapshot meaning: The company owes $6.55M within 12 months. Investors see this as near‑term cash that must leave the business — a key part of runway analysis.

Vendor leverage: $2.1 M in payables represents short‑term supplier financing — in effect, the company is borrowing time and credit from vendors.

Borrowing dependency: Short‑term loans ($1.8 M) may need rolling over soon; monitor refinancing risk and interest cost trends.

Deferred revenue: $450 K acts as customer‑funded working capital — the company already has cash but must still deliver services.

Healthy structure: Compare Current Assets vs. Current Liabilities (→ Current Ratio or Quick Ratio) to gauge liquidity.

Watch signals:

Consistent stretch in Accounts Payable → may indicate deliberate cash management or mounting strain.

Rising accrued expenses > revenue growth → flag for expense recognition timing.

For founders: Align payment schedules with cash inflows; avoid short‑term debt buildup that compresses runway unexpectedly.

For investors: Check if increased current liabilities are funding growth efficiently (positive leverage) or masking cash flow pressure.

Worked Example

Current Liability Item | Amount | What It Represents |

|---|---|---|

Accounts Payable | $2,100,000 | Outstanding supplier invoices for goods/services already received |

Short-term Borrowings | $1,800,000 | Revolving credit lines and overdrafts due within 12 months |

Current Portion of Long-term Debt | $900,000 | Principal repayments on term loans due this year |

Accrued Expenses | $650,000 | Accrued bonuses, payroll, utilities, and interest payable |

Taxes Payable | $300,000 | Corporate, payroll, or sales taxes owed but unpaid |

Deferred Revenue (current) | $450,000 | Customer prepayments for services to be delivered within 12 months |

Current Lease Liabilities | $200,000 | Lease payments due in the next 12 months |

Other Current Liabilities | $150,000 | Miscellaneous short-term obligations (e.g., legal or warranty claims) |

Total Current Liabilities | $6,550,000 | Commitments due within the next year |

Notes:

Snapshot meaning: The company owes $6.55M within 12 months. Investors see this as near‑term cash that must leave the business — a key part of runway analysis.

Vendor leverage: $2.1 M in payables represents short‑term supplier financing — in effect, the company is borrowing time and credit from vendors.

Borrowing dependency: Short‑term loans ($1.8 M) may need rolling over soon; monitor refinancing risk and interest cost trends.

Deferred revenue: $450 K acts as customer‑funded working capital — the company already has cash but must still deliver services.

Healthy structure: Compare Current Assets vs. Current Liabilities (→ Current Ratio or Quick Ratio) to gauge liquidity.

Watch signals:

Consistent stretch in Accounts Payable → may indicate deliberate cash management or mounting strain.

Rising accrued expenses > revenue growth → flag for expense recognition timing.

For founders: Align payment schedules with cash inflows; avoid short‑term debt buildup that compresses runway unexpectedly.

For investors: Check if increased current liabilities are funding growth efficiently (positive leverage) or masking cash flow pressure.

Best Practices

Monitor liquidity ratios: Track Current Ratio (Current Assets/ Current Liabilities and Quick Ratio (Cash + Receivables / Current Liabilities) to gauge short‑term solvency.

Reconcile timing: Regularly align accrued and payable balances with actual payment cycles to avoid hidden obligations.

Separate financing vs. operating: Distinguish operational liabilities (payables, accruals) from short‑term financing (loans, overdrafts) — investors analyze them differently.

Cash forecasting: Build a simple week‑by‑week cash flow plan that includes all upcoming payments from your current liabilities—like supplier invoices, taxes, and short‑term debt. This helps you see when cash will leave the business and whether you’ll have enough liquidity to cover each week’s obligations.

Compare trends: Rising current liabilities with flat current assets → tightening liquidity; balanced growth indicates healthy working‑capital rotation.

Best Practices

Monitor liquidity ratios: Track Current Ratio (Current Assets/ Current Liabilities and Quick Ratio (Cash + Receivables / Current Liabilities) to gauge short‑term solvency.

Reconcile timing: Regularly align accrued and payable balances with actual payment cycles to avoid hidden obligations.

Separate financing vs. operating: Distinguish operational liabilities (payables, accruals) from short‑term financing (loans, overdrafts) — investors analyze them differently.

Cash forecasting: Build a simple week‑by‑week cash flow plan that includes all upcoming payments from your current liabilities—like supplier invoices, taxes, and short‑term debt. This helps you see when cash will leave the business and whether you’ll have enough liquidity to cover each week’s obligations.

Compare trends: Rising current liabilities with flat current assets → tightening liquidity; balanced growth indicates healthy working‑capital rotation.

FAQs

What’s the difference between current and non‑current liabilities?

Current liabilities are due within 12 months (or one operating cycle). Non‑current liabilities are obligations due after that period — long‑term debt, leases, deferred taxes, etc.Why do current liabilities matter to investors and founders?

They determine short‑term cash flexibility. Startups with large payables or short‑term loans might appear liquid but could face near‑term repayment stress if not managed carefully.Does deferred revenue count as a current liability?

Yes — the portion tied to goods or services deliverable within a year. Longer commitments go under non‑current.Can current liabilities ever be “good”?

Absolutely. Efficient use of supplier credit or short‑term debt can optimize working capital and boost cash flow — as long as it’s deliberate and backed by sufficient current assets.How do changes in current liabilities affect cash flow?

An increase (e.g., higher payables or accruals) → cash inflow in the short term (delayed payments).

A decrease → cash outflow (paying off obligations).

This is a critical bridge between net income and operating cash flow.

FAQs

What’s the difference between current and non‑current liabilities?

Current liabilities are due within 12 months (or one operating cycle). Non‑current liabilities are obligations due after that period — long‑term debt, leases, deferred taxes, etc.Why do current liabilities matter to investors and founders?

They determine short‑term cash flexibility. Startups with large payables or short‑term loans might appear liquid but could face near‑term repayment stress if not managed carefully.Does deferred revenue count as a current liability?

Yes — the portion tied to goods or services deliverable within a year. Longer commitments go under non‑current.Can current liabilities ever be “good”?

Absolutely. Efficient use of supplier credit or short‑term debt can optimize working capital and boost cash flow — as long as it’s deliberate and backed by sufficient current assets.How do changes in current liabilities affect cash flow?

An increase (e.g., higher payables or accruals) → cash inflow in the short term (delayed payments).

A decrease → cash outflow (paying off obligations).

This is a critical bridge between net income and operating cash flow.

Related Metrics

Commonly mistaken for:

Non‑current liabilities (timing difference)

Total debt (includes both short‑ and long‑term borrowings)

Related Metrics

Commonly mistaken for:

Non‑current liabilities (timing difference)

Total debt (includes both short‑ and long‑term borrowings)

Source of:

Index